In the second part, our topic is finance and insurance because even by choosing a bank and investing your money sustainably you can change the world.

Why is this relevant?

We pay attention to sustainability in food, fashion, and transport – why then not also in banks and insurance providers? These institutions in particular could decisively accelerate or block sustainable development. According to the Federal Environment Agency, they contribute a considerable share to climate change and are thus jointly responsible.

What can I do?

- Inform yourself about the investments and policies of your bank and insurance company

- As a bank and insurance customer, get banks and insurance companies to rethink their policies.

- Switch to a fair bank (examples follow)

- Switch to a fair insurance company

- Invest money in fair funds

Just in Germany, banks and insurers invested nearly $10 billion in nuclear weapons producers between 2014 and 2017 [1].

“Don’t bank the bomb”, ICAN, PAX, 2018

Banks

1. The Problem

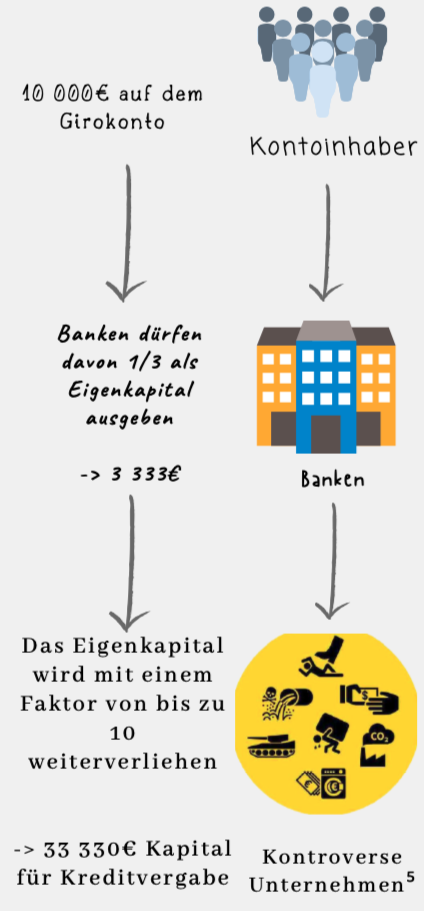

2/3 of the greenhouse gases emitted by industry since the Industrial Revolution can be attributed to 90 companies. These are pressured by the investments of banks as shareholders or by the granting of loans to generate the highest possible profit as quickly as possible. Sustainable behaviour is hardly feasible under this premise. Thus, all the passive money of the customers, even if it is only in the current account, is invested without consent in, among other things, the arms industry, foodstuffs such as grain or palm oil, coal and mining!

2. My bank too?

99,3% yes, unless you are already a customer of a sustainability bank. Without exception, the conventional banks invest in fossil fuels, weapons, companies that disregard human rights, etc. [1] A few memorable examples: Sparkasse invested 2.1 billion in weapons companies within 2 years [3], Volks- und Raiffeisenbank invests in nuclear weapons [2], Deutsche Bank or Postbank invested 68.8 billion in fossil fuels in only 3 years and Commerzbank provided funds used for nuclear intercontinental missiles [4]. More information can be found at www.fairfinanceguide.de

[1] https://www.fairfinanceguide.de/%C3%BCber-uns/

[2] ICAN atombombengeschaeft.de/diese-banken-investieren/

[3] www.facing-finance.org/files/2019/05/ff_dp7_ONLINE_v02.pdf

[4] https://www.sueddeutsche.de/wirtschaft/commerzbank-waffen-kohle-elternzeit

3. Are there alternatives?

No. There are several so-called “sustainability banks” such as GLS Bank, Triodos Bank, Umweltbank, Ethik Bank, all of which have been rated as very good by the NGO Facing Finance with only minor differences [1](see facing-finance.org). At a sustainability bank, account management usually costs between €5-10 per month, but there is also often a “young people’s discount”.

In return, you get a bank that does not invest in fossil fuels and makes sure that its investments do not promote child labour.

Insurances

1. How insurances work?

Insurance is used to protect against risks and to cover financial losses. They are based on the so-called “collective assumption of risk”. Companies also need cover, as economic actions can lead to a financial loss. Premiums and fees are used to pay the claims of all insured persons, but also to invest capital. In addition, insurance companies are reliable providers of capital for financing companies, real estate and banks. In Germany, insurers are among the largest institutional investors.

2. How sustainable are insurances?

surance companies are important investors and are responsible for the protection of companies. Through their investments and hedges, they support, for example, nuclear weapons producers [1] or fossil energy operators [2]. Thus, insurance companies can block the sustainable development of society through their capital flows. In recent years, a positive trend can be seen: many large insurers have reduced their coal business and are investing more and more in renewable energies [3,4]. Choosing sustainable and fair insurance or encouraging large insurers to rethink is therefore an important step towards a more sustainable society.

Sustainable and fair insurance companies have strict criteria for their investments (e.g. no investments in armaments, nuclear power) and are usually more transparent. Some also work ecologically (green buildings, public transport promotion)[5].

[1] “Don’t bank the bomb”, ICAN, PAX , 2018

[2]”Insure Coal no more”, Unfriend Coal, 2019

[3] https://www.energiezukunft.eu/wirtschaft/mehr-versicherungen-ziehen-sich-aus-dem-kohlegeschaeft-zurueck/

[4] GDV “Fakten zur Versicherungswirtschaft”, 2019

[5] https://utopia.de/ratgeber/nachhaltige-versicherung-gruene-rente-krankenkasse/

[6] FairFinance Guide Deutschland, 2019 https://www.fairfinanceguide.de/

Sustainable and fair insurances (examples)

- Statutory health insurance: BKK24, BKK Provita

- Private health insurance: Securvita BKK

- Liability insurance: Greensurance, Mehrwert

- Vehicle insurance and pension insurance: Barmenia Insurances, Concordia Oeco, Pangae Life, Waldenburger Versicherung

Funds

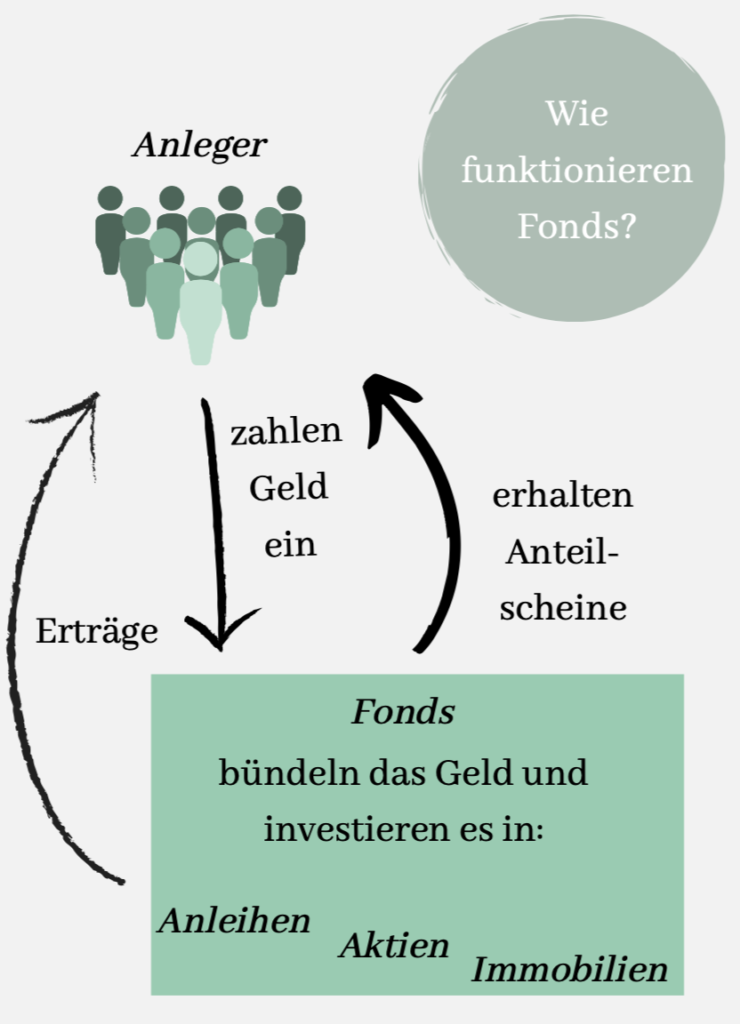

1. What are green funds?

Green funds are sustainable investments. They invest in companies and projects that take ecological, social and ethical aspects into account. For example, industries such as nuclear power, genetic engineering or weapons are excluded from the outset [3].

2. What to look out for?

Lower dividend?

Overall, no lower profitability can be observed for green funds than for regular ones. Christoph Lützel from GLS Bank summarises this as follows: “If you go back, so the last few years have been excellent in terms of returns. Really good. Of course, prices are volatile, which means they can go down sometimes. But overall we are doing very well. And there is no reason to avoid these green funds or GLS Aktienfonds, for example. Because these are values that focus on the future, on sustainability, ecology and social issues. That is the future, that has yield and that has perspective.” [1]

Truly sustainable?

How sustainable green funds really are is often difficult to discern and depends on one’s own interpretation of sustainability. Due to sometimes very entangled corporate networks, it is not always easy to understand which companies participate in which projects [1]. Sustainability and moral value are not protected, clearly defined terms; rather, they depend on the subjective attitude of the individual. Companies are often not sustainable on all criteria [2]. Therefore, one should decide for oneself what is important or still acceptable to one. It is helpful to work with negative-positive criteria, i.e. to determine what the company should not be involved in under any circumstances or what should be promoted in any case [1].

Appropriate for students?

ETF savings plans are particularly suitable for young people. The earlier you start investing your assets, the better. ETF savings plans can be started from as little as €25 [4].

[1] Grüne Banken https://www.br.de/radio/bayern1/gruene-banken-100.html

[2] Finanztip Nachhaltige Geldanlagen https://www.finanztip.de/indexfonds-etf/nachhaltige-geldanlagen/

[3] Ethisch-ökologische Investmentfonds https://www.geld-bewegt.de/wissen/geld-versicherungen/nachhaltige-geldanlage/ethischoekologische-investmentfonds-15953

[4] ETF-Sparplan für Studenten https://www.finanz-kroko.de/etf-sparplan-fuer-studenten/